Beverly Hills famously has some of the country's most valuable real estate. On the western end of the city, between the Los Angeles Country Club and North Beverly Drive, the median home value is about $3 million, according to real estate website NeighborhoodScout.com, and many properties cost far more. This posh neighborhood in the 90210 zip code is lined with pristine single-family homes, most with at least four bedrooms.

Streets need not be filled with big estates to have high home values. On the opposite coast, in Manhattan, an area bordering the east side of Central Park from 70th Street to 77th Street, between Park Avenue and Fifth Avenue, contains homes with a median value of $2.8 million. (In comparison, the median home value citywide is about $779,000, estimates NeighborhoodScout.) Unlike Beverly Hills, the area is mostly stacked with luxury apartments, according to data from the U.S. Census Bureau's 2005-2009 American Community Survey.

Size and style can determine much of a home's value, but other factors can weigh more heavily. Within a single city, the prices of similar homes can display huge differences depending on the area-and even the street-in which they are located. The two key drivers of value are access to work opportunities and access to amenities, says Andrew Schiller, founder and chief executive of NeighborhoodScout.com. A few streets' distance can make a difference in perceived proximity to school districts, recreational amenities, and transportation routes.

No. 1: Access to Job Opportunities

Areas with the most expensive real estate in any city are often close to places with high paying jobs. Within them, the most expensive streets typically have larger homes that are closer to local amenities. Affluent homebuyers may seek big homes with views in good school districts. For primary residences, however, "access to opportunity is so significant that even if homes are smaller, the values [in an area] can still go up," Schiller says. "People will put up a lot to make a lot of money and support their families."

To determine the most expensive neighborhood in each state, NeighborhoodScout estimated the median home values in third quarter 2010 for about 62,000 census tracts, or county subdivisions, across the U.S. The ranking includes only places with more than 800 residents and with at least one-fourth of properties occupied by owners, rather than rented. This excludes certain subdivisions and small towns known to have very high property values.

In addition to parts of Beverly Hills and Manhattan's Upper East Side, other expensive places include Port Royal, Fla., (which has waterfront homes along the ocean, canals, and bay), Alpine, N.J. (a suburb of Manhattan that attracts many celebrities and business executives), and the Golden Triangle section of Greenwich, Conn. (where incomes are among the nation's highest). Values range from $266,293 in Fargo, N.D., to more than $3 million in Beverly Hills. In nearly every state, the most expensive areas are near water, hills or mountains, parks, or country clubs.

Beauty Rates in Second-Home Markets

While Beverly Hills and Manhattan provide access both to urban centers with high-paying jobs as well as amenities, home values in other exclusive neighborhoods are heavily propped up by just one of these factors.

Buyers in second-home markets such as Port Royal, Block Island, R.I., or Big Sky, Mont., for example, pay a premium for such amenities as views, waterfront, and outdoor recreation. Some of the most expensive properties in Block Island are on the waterfront. "People are not moving there to get great jobs," says Schiller.

High-end markets tend to hold their values better than average ones, but even the most exclusive areas are vulnerable to economic distress. Arizona's affluent community of Paradise Valley, for instance, has not been hit as hard as the rest of the state because many residents withstood the stress of the recession relatively well, says Bob Hassett, a broker at Russ Lyon Sotheby's International Realty. Still, values in the area have declined by more than 25 percent in the last two years, estimates NeighborhoodScout.

Amenities Can Lose Value

Schiller warns that places relying on amenities to sustain home values can be more vulnerable to price drops during an economic downturn than those that are near job centers. For instance, NeighborhoodScout estimates that home values in Port Royal have dropped by about 21 percent in the last two years, compared with a relatively minor dip of 5.52 percent in Chevy Chase Village, Md., a wealthy suburb of Washington, one of the most stable metro job markets.

Exclusive communities migrate over the years as opportunities shift to new places. Beverly Hills did not develop until movie stars began moving there in the early 1900s, according to the city's website. While the most expensive place in Texas is currently the Afton Oaks-River Oaks section of Houston, whose median home value is about $1.7 million, Schiller predicts that prices in Austin will rise as government activity, job growth, and the University of Texas attract more homebuyers to the area.

Neighborhoods near Austin and other emerging cities may not be expensive now, but the right combination of amenities and job opportunities might one day push them to the top of the price ladder.

Here's America's Top 10 Most Expensive Blocks:

|

Kenilworth, IL

Map: US Census Bureau |

No. 10 Kenilworth, IL

Where: Ridge Road to Lake Michigan

Median home value: $1,610,824

Median household income: $247,000

Kenilworth, one of the most affluent towns in the country, is the most expensive neighborhood in which to buy a home in Illinois. Homes by Lake Michigan can cost several million dollars: For example, a seven-bedroom home at 245 Sheridan Road is listed for $6.5 million, according to Zillow.com.

Note: For all 10 the median home value source is NeighborhoodScout.

|

Chevy Chase Village, MD

Map: US Census Bureau |

No. 9 Chevy Chase Village, MD

Where: Chevy Chase Country Club to Western Avenue

Median home value: $1,677,640

Median household income: $250,000+

Chevy Chase Village, located on the border of Maryland and Washington, D.C., is one of the most expensive real estate markets in the country. The area is known for Victorian and colonial style homes, according to theestridgegroup.com.

|

Town Center, Great Falls, Va

Map: US Census Bureau |

No. 8 Town Center, Great Falls, VA

Where: Seneca Road to Georgetown Pike

Median home value: $1,721,441

Median household income: $193,214

This upscale residential neighborhood was named after the Potomac River’s Great Falls, which drops 75 feet over a two-mile distance. Home prices start in the mid-$400,000s and exceed $8 million for large estates in such areas as Clarks Branch, Potomac Ridge Estates, Falcon Ridge, and Rossmore, according to greatfalls-realestate.com.

|

Afton Oaks/River Oaks, Houston, TX

Map: US Census Bureau |

No. 7 Afton Oaks/River Oaks, Houston, TX

Where: Buffalo Bayou to San Felipe Street

Median home value: $1,722,454

Median household income: $250,000+

Streets around the River Oaks Country Club, such as Inwood Drive and Lazy Lane, have some of the most expensive estates in this section of Houston, according to estimates on Zillow.com. River Oaks is also home to the Menil Collection, a museum of modern art created by Schlumberger oil-drilling heiress Dominique De Menil and her husband Jean. The building, featuring designs by both Louis Kahn and Renzo Piano, houses nearly 16,000 works, including antiquities, Byzantine, African, and Modern art. One of the highlights is the Mark Rothko chapel.

|

Honolulu, HI

Map: US Census Bureau |

No. 6 Honolulu, HI

Where: Around the Diamond Head State Monument

Median home value: $1,912,135

Median household income: $95,625

The Diamond Head community is a short walk from the main shopping and restaurant area of Waikiki. One street known for luxury real estate is Kahala Avenue, says Mike Bates, a real estate associate for Coldwell Banker Pacific Properties. Along Diamond Head Road, a street that wraps around the peak, are beachfront properties as well as hillside homes on such streets as Noela Street and Diamond Head Circle.

|

Golden Triangle, Greenwich, CT

Map: US Census Bureau |

No. 5 Greenwich, CT

Where: Golden Triangle

Median home value: $2,214,072

Median household income: $250,000+

The Golden Triangle section of Fairfield County’s affluent community of Greenwich includes the Greenwich Country Club. According to Barbara Wells, a real estate agent for Prudential CT Realty, Meadowcroft Lane is the most expensive street in the area.

|

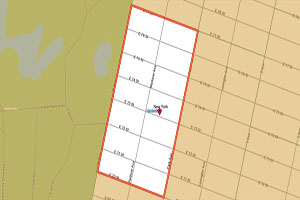

Alpine, NJ

Map: US Census Bureau |

No. 4 Alpine, NJ

Where: Anderson Avenue to Hudson River

Median home value: $2,440,719

Median household income: $167,917

Many celebrities and executives, such as Russell Simmons and Eddie Murphy, have lived in Alpine, an exclusive community with large private estates. Among the most expensive properties for sale is this mansion, listed for $68 million, according to realtor.com.

|

Port Royal, Naples, FL

Map: US Census Bureau |

No. 3 Port Royal, Naples, FL

Where: Gulf Shore Boulevard to tip of Port Royal

Median home value: $2,703,453

Median household income: $139,250

Waterfront properties are abundant in Port Royal, on the southern tip of Naples between the Gulf of Mexico and Naples Bay. Water views and private docking in the canals make it one of the country’s most exclusive communities. According to Naples real estate agent John Tsiskakis, some of the most expensive streets include Gulf Shore Boulevard, Gordon Drive, Galleon Drive, Rum Row, and Fort Charles Drive.

|

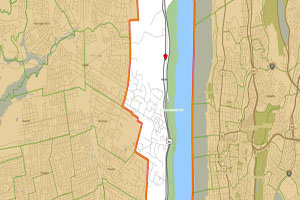

Upper East Side, Manhattan, NY

Map: US Census Bureau |

No. 2 Upper East Side, Manhattan, NY

Where: 70th St. to 77th St. between Park Ave. and Fifth Ave.

Median home value: $2,801,925

Median household income: $229,632

These streets east of Central Park along Fifth Avenue, Madison Avenue, and Park Avenue are lined with historic townhouses and co-ops built during the turn of the 20th century and the 1930s. Many homes along Fifth Avenue have park views. Museums, shopping, and dining are a few blocks away.

(Note: Some other expensive neighborhoods in New York were not included because they did not meet the minimum population requirement for this ranking.)

|

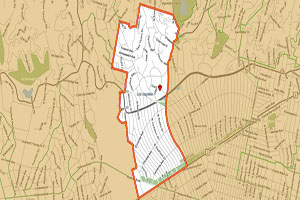

Beverly Hills, CA

Map: US Census Bureau |

No. 1 Beverly Hills, CA

Where: North Wittier Drive to North Beverly Drive

Median home value: $3,067,119

Median household income: $167,583

Bordered on the west by the Los Angeles Country Club, this area has the highest median home values in the Beverly Hills area, according to NeighborhoodScout. Cliff Nichols, general manager at the brokerage Hilton & Hyland, says Lexington Road is one of the area's most expensive streets. Among the priciest homes for sale: the Pickfair Estate—home of silent movie stars Mary Pickford and Douglas Fairbanks—at 1143 Summit Drive, 90210, which is listed for $60 million.